Alibaba Stock: Buy, Sell, or Hold?

Alibaba Group (NYSE: BABA) has had a rough time recently, with the stock down nearly 60% over the past five years. However, billionaire co-founder Jack Ma recently praised the company and its restructuring efforts. Ma said that while mistakes have been made in the past, the decision to split the company into six divisions has led it to become more agile and customer-focused.

Let's look at Alibaba's prospects and if the stock is currently a buy, sell, or hold.

A free-cash-flow machine

Despite its struggles, the one thing Alibaba has consistently been able to do is produce a tremendous amount of cash flow. For its fiscal third quarter, ended in December, it generated operating cash flow of $9.1 billion and free cash flow of $8 billion. Through its first nine months of the year, the company produced $22.4 billion in operating cash flow.

Strong cash flow is important as it gives companies a lot of flexibility. They can reinvest it to reinvigorate growth in the company, or use it to make acquisitions. The cash can also be used to buy back shares.

Alibaba has been aggressive on the share repurchase front, announcing a $25 billion share buyback program in conjunction with its fiscal Q3 results in February. The company quickly acted on the repurchase authorization, buying back $4.8 billion in shares in the first three months of 2024. Alibaba has now repurchased $23.3 billion in shares over the past two years.

Alibaba is also looking to invest in its two core businesses, e-commerce and cloud computing, to reignite growth. For its e-commerce business, Alibaba is looking to invest in price competitiveness, service, and user experience. Improving product supply and adding more branded and direct-from-manufacturer products to its platform will be a key initiative that will include offering flexible models to suppliers so they can offer their products at the best prices.

The company is also investing in the customer experience from presale to logistics. In addition, Alibaba is in the early days of testing its own internally developed large language model (LLM) for artificial intelligence (AI) to help improve its search and advertising capabilities.

For its cloud computing business, Alibaba is looking to move customers away from low-margin project-based contracts toward its public cloud offering. The company is increasing investment in AI-related hardware and software and scaling out infrastructure to support AI-driven computing power demand.

Still some risks ahead

Chinese companies are more limited with AI given U.S. bans on the latest GPU technology from Nvidia and others, so Alibaba may not see the same immediate benefit that U.S. cloud computing companies like Microsoft and Alphabet are seeing. At the same time, Alibaba cut cloud computing prices to lure AI developers to its data center offering. So while AI has some long-term potential, it could be a bit of a headwind in the near term.

Alibaba's e-commerce business, meanwhile, has also had to invest in price given the strength of rival PDD Holdings and its popular Pinduoduo platform that has been rapidly taking share. PDD's success has led the Chinese e-commerce market to become even more competitive, although Alibaba's T-Mall and Taobao platforms are still two of the strongest e-commerce sites in the country and tend to do well at the higher end.

A lackluster Chinese economy coming out of pandemic lockdowns has also weighed on Alibaba's results. The Chinese economy did pick up in the first quarter, and the Chinese government has indicated it will take measures to support the economy. Any rebound in the Chinese economy should be good for Alibaba, although risks remain.

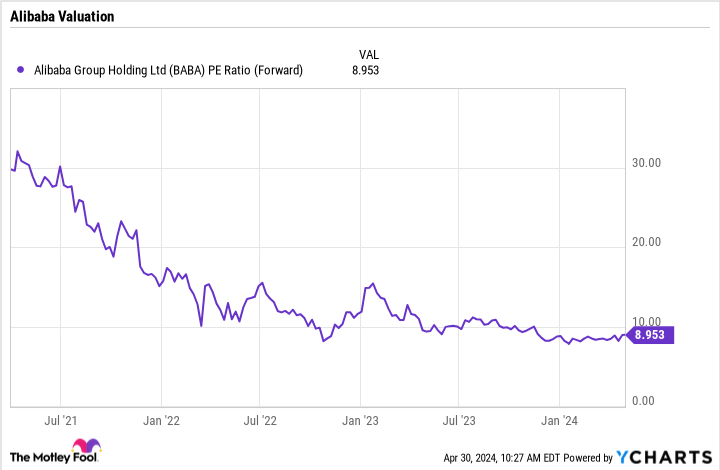

A very cheap stock

One of the big things that sticks out with Alibaba is its valuation. Trading at just about a 9x forward P/E ratio, the stock is very cheap for a company that has grown its revenue by 9% over the past nine months and is generating a lot of cash flow.

Now, a cheap valuation is not reason enough to buy a stock, as it could be a value trap. However, Alibaba is a cheap stock of a leading Chinese company that generates a prolific amount of cash that it is using to buy back shares and invest in its business to reignite growth. While the stock does come with risks, its upside over the next several years looks intriguing given these characteristics. As such, Alibaba stock is a buy right now.

Should you invest $1,000 in Alibaba Group right now?

Before you buy stock in Alibaba Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alibaba Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $544,015!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 30, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Geoffrey Seiler has positions in Alibaba Group and Alphabet. The Motley Fool has positions in and recommends Alphabet, Microsoft, and Nvidia. The Motley Fool recommends Alibaba Group and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Alibaba Stock: Buy, Sell, or Hold? was originally published by The Motley Fool